![Signals From [Space]](https://substackcdn.com/image/fetch/w_80,h_80,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F55686857-6b99-45a6-ac0f-09c9f023f2a0_500x500.png)

![Signals From [Space]](https://substackcdn.com/image/fetch/e_trim:10:white/e_trim:10:transparent/h_72,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F4d588ac1-7fac-4bd4-829d-fc7b4e8f1326_1512x288.png)

![Signals From [Space]](https://substackcdn.com/image/fetch/w_36,h_36,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F55686857-6b99-45a6-ac0f-09c9f023f2a0_500x500.png)

Visual Update: Kidney Capital's Most Active Investors & Segments

Data from 14 of the most active investors from idea to IPO

Late last year I sent out version one of my Most Active Investors table. My goal then, as it is now, was to paint a picture of funding trends, patterns, and critical gaps across the kidney care ecosystem.

The first installment of this “Kidney Capital” series focused on three themes: CVS entering care delivery, Baxter’s early plans around Vantive (before the recent course change), and why Y Combinator was starting to back more bio and health startups.

The second part of the series took us straight into “death valley.” For many startups, even after they earn their first outside capital (usually grants), they face significant funding hurdles to reach their next product, research, and business milestones. Sometimes to the tune of tens of millions of dollars. As you might imagine from it’s name, many do not survive.

Today, I’m updating our visual ahead of the soon-to-be-launched part three, which focuses on a few new themes that have bubbled to the surface in 2024 — this includes most of our favorite three-letter acronyms like VBC, LDO, and IPO.

Request for Feedback

Please take a moment to review the graphic below. Keep in mind this is a select group of companies and investors. It is not meant to be exhaustive. If that’s what you’re looking for, you’ll find it in my data room below.

If you have insights, tips, or takeaways to share on the current funding climate and what we should expect to see in this portfolio over the next 12 to 24 months, please hit reply or send me an anonymous note.

What's in this table:

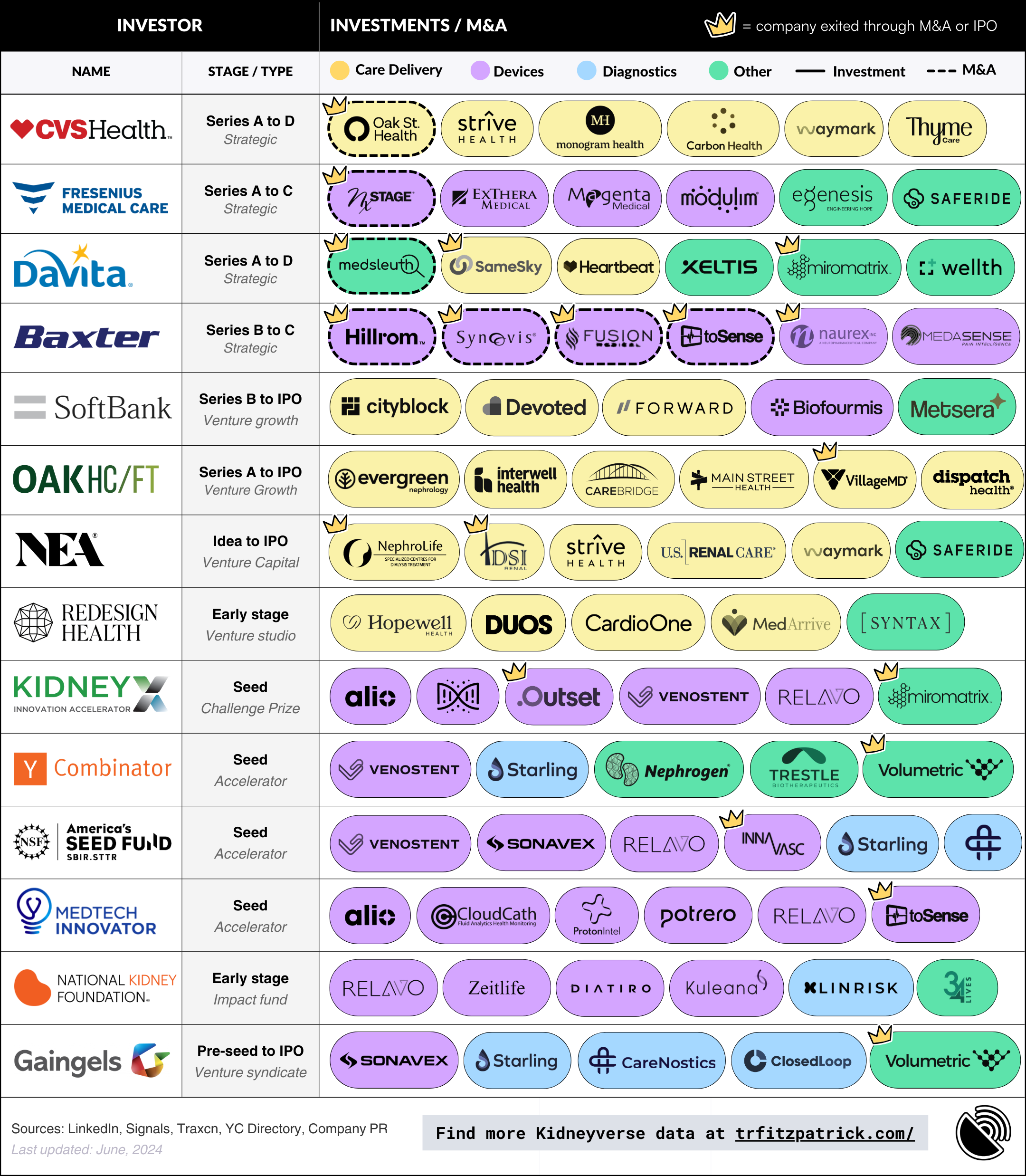

Who & When: The left-most columns in this table contain 14 of the most active investors in kidney care across the company lifecycle. This group broadly represents four investor types from idea to IPO: (a) accelerators; (b) early stage venture capital; (c) growth equity; and (d) strategic capital.

What: There are 4 segments (colors) highlighted in this table: Care delivery (yellow), devices (purple), diagnostics (blue), and other (green). For what it’s worth, I track 9 segments across the Kidneyverse.1

Why: Investments happen because founders and investors share a unique point of view about what the future looks like. It’s as much about timing (why now?) as it is about fit (why you?). First, I’ve separated investments (solid border lines) from mergers & acquisitions (dotted lines). Second, I’ve included a crown (“👑”) for companies with an exit, either through M&A or IPO.2

What’s new:

First, you'll notice we've added three new investors to the mix. My goal here is to highlight three different strategies within the venture landscape in (a) growth (SoftBank); (b) early stage (New Enterprise Associates (NEA), and (c) venture studio (Redesign Health).

I've also added updated portfolio companies within the existing investor categories. Many of you called out these companies after I published v1.0 in December, especially in light of recent headlines (breakthroughs, M&A, etc.). These include eGenesis, Inc., Thyme Care, Heartbeat Health, SameSky Health, and 34 Lives to name a few.

Discussion

What are you seeing and hearing in this space right now? We've continued to see consolidation in care delivery, and are starting to see it among specialty value-based care delivery (though, outside of kidney for now). A big question on my mind is how / when some of these late stage investors who see the full picture (say polychronic, in-home, or tech-enabled care) decide to start selling, buying, or merging their bets. With many billions at work in this the yellow bubbles alone, and continued "resets" in areas like virtual, primary, and VB care, I think it's fair to expect some moves in this space over the next 6 to 12 months.

Please know my inbox is always open, and Kidneyverse Careers exists to help you find your next role or key hire.

Thank you for being here, and stay tuned.

— Tim

Want to support my work?

The “Other” group in this post (green) contains multiple segments. This post focuses on the first three segments given their outsized attention in private markets. Learn more about all 9 subsegments in the Kidneyverse.

The goal of separating invest-ments from exits, and invest-ors from acquirers is to underscore the importance of fit in investor decision making. This includes problem-solution fit, product-market fit, and strategic fit.

Founders pitch hundreds of potential investors to find the one or two that say “yes” and get to conviction on that shared point of view. On the flipside, investors hear thousands of pitches and invest in only a handful.